Mission

The mission of the Finance Department is to provide responsive, professional, and ethical administrative and fiscal services to meet the needs of the public, City Council, and all city departments. We value and maintain business practices that further the city’s sustainability and development goals.

Responsibilities

The Finance Department is responsible for planning, directing and administering the major functions of accounting, budgeting, financial reporting, employer insurance management employee benefits, internal audit, financial documents, and central payment processing.

Tax Bill Breakdown

Welcome to our Tax Bill Breakdown widget, where you will get a clear understanding of how your tax dollars are being used to enhance our City of Kaukauna community.

To find out what your property is paying to each of the categories, search for your address:

Learn More About

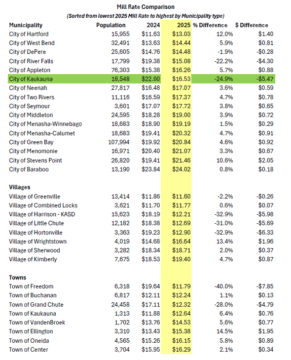

Each year, residents ask how Kaukauna’s mill rate compares to neighboring communities. This section provides a clear, annual comparison to help property owners see how Kaukauna aligns with the Fox Valley and other similar-sized Wisconsin cities.

What Is a Mill Rate?

A mill rate reflects the tax owed per $1,000 of a property’s taxable assessed value.

Example: A mill rate of 16.00 means a property owner pays $16.00 for every $1,000 of assessed value.

Mill rates are a helpful comparison tool from community to community, but they do not tell the full story of why one community’s taxes differ from another.

Where to Find the Mill Rate on Your Tax Bill

Every Wisconsin property tax bill lists the mill rate for each taxing jurisdiction.

Look for the line labeled “Net Assessed Value Rate.”

Multiply this number by $1,000 to convert it to dollars and cents.

Mill Rate Comparison Table

This table focuses on two comparison groups: surrounding communities, and similar-sized municipalities that are likely to provide comparable levels of service.

How to Interpret Mill Rates

While a higher mill rate generally means higher taxes, mill rates alone do not indicate whether a community is more or less expensive to live in. Municipalities structure their budgets differently, and not all communities include the same services in their tax rate.

Mill rates vary based on:

- Services provided (police, fire, parks, streets, libraries)

- Infrastructure and capital investments

- Mix of residential, commercial, and industrial property

- Long-term debt strategy and financial planning

- Community priorities and growth initiatives

Because of these differences, mill rates reflect not just tax levels but also the service model, amenities, and financial decisions unique to each community. When comparing mill rates, it’s important to consider what is included in the rate and whether those services align with a property owner’s expectations and values.

The Wisconsin Department of Transportation (WisDOT) collects the City of Kaukauna’s vehicle registration fee, commonly referred to as the wheel tax, at the time of vehicle registration and each annual renewal. WisDOT retains a small administrative fee (approximately three cents per vehicle application) and remits the remainder to the City. When applicable, your vehicle registration certificate will indicate that a municipal and/or county vehicle registration fee was paid.

Revenue from the vehicle registration fee generates approximately $150,000 annually and is accounted for separately in Fund 221 – Vehicle Registration Fee Fund. These funds are used to help pay for road construction and transportation infrastructure.

In most new street projects, costs are shared between the City and adjacent property owners, with the City typically covering one-third of the cost and property owners collectively covering the remaining two-thirds. Corner lots, which have frontage on two streets, would otherwise face higher costs; City ordinance includes a formula that limits their financial exposure to maintain fairness. As a result, the City assumes a greater share of costs in these situations, and vehicle registration fee revenue helps offset that expense.

Without the vehicle registration fee, these road-related debt costs would need to be absorbed by the general property tax levy. The intent of the fee is straightforward: drivers directly benefit from local streets, bridges, sidewalks, and transportation infrastructure, and this fee ensures that those users contribute toward those costs. Wisconsin law requires that vehicle registration fee revenue be used only for transportation-related purposes, such as road maintenance and snow removal. It is one of the limited tools available to municipalities to fund transportation needs while reducing pressure on property taxes.

Vehicle Registration Fee (Wheel Tax) – Frequently Asked Questions

What is the vehicle registration fee (wheel tax)?

The vehicle registration fee, often called a wheel tax, is a small annual fee added to the standard Wisconsin vehicle registration for vehicles that are kept in the City of Kaukauna. It is authorized under Wisconsin law and collected by the Wisconsin Department of Transportation (WisDOT) on behalf of the City.

How much is the fee and when is it collected?

The City of Kaukauna’s vehicle registration fee is $10 per vehicle per year. WisDOT collects the fee when a vehicle is first registered and again each year at renewal. The fee appears as a separate line item on your registration renewal notice.

Who has to pay the fee?

The fee applies to eligible vehicles (such as automobiles and light trucks) that are customarily kept within the City of Kaukauna. Vehicles kept outside the city limits are not subject to the fee.

Who collects the fee and where does it go?

WisDOT collects the fee along with your regular registration and sends the revenue to the City, retaining only a small administrative charge. The funds are deposited into a separate City account dedicated solely to transportation-related costs.

What is the money used for?

Vehicle registration fee revenue is used to help pay for local road construction, road-related debt, and transportation infrastructure. This includes situations where the City must cover a larger share of road costs, such as limiting the financial burden on corner lots through City ordinance.

Why does the City charge this fee instead of using property taxes?

Without the vehicle registration fee, road construction and debt costs would need to be funded through the property tax levy. The fee helps shift a portion of these costs to drivers who directly use and benefit from city streets, reducing pressure on property taxes.

Can the City use this money for other services?

No. Wisconsin law requires that vehicle registration fee revenue be used only for transportation-related purposes, such as road maintenance, construction, and snow removal. It cannot be used for general City operations.

Why do some communities have this fee and others don’t?

State law allows municipalities to adopt a vehicle registration fee, but it is a local policy decision. Communities choose whether to use this tool based on their transportation needs and financial structure.

The City of Kaukauna uses Municipal bonds to finance capital projects including streets, equipment, sewer systems, and buildings. Municipal bonds are debt securities. Generally, the interest on municipal bonds is exempt from federal income tax. The city typically borrows for projects for a 1-3 year span of projects. The list of projects on the 5-year capital improvement plan (CIP) can be found here. These are the projects that will have Municipal bonds issued in the future.

Many factors go into a municipal bond financing deal. The City is rated each time it goes to market for a bond offering. The rating gives the bond market an indication of how well the city is doing and if the bonds they are issuing are a risky investment. The company used by the City to do the rating is S&P Global Ratings. This company provides the third party rating basing its rating on many different criteria. The better the rating the safer the investment is for the investors. In turn, a better interest rate to the city to borrow the funds.

The City is currently rated at a AA- with a Stable outlook. With the below high-level criteria comments.

- Strong economy in the broad and diverse Appleton metropolitan statistical area, highlighted by robust valuation gains, which is offset somewhat by weaker incomes

- Very strong reserves and liquidity, supported by stable operating performance, which is expected to continue

- Weak debt and contingent liability profile with elevated debt service, with a well-funded pension plan

- Adequate financial management with standard financial policies and practices under our Financial Management

- Assessment methodology, with a five-year capital improvement plan; and a strong institutional framework score

Link to the latest full Report – S&P Report

City Finance collaborates with each department and stakeholders to create a budget where it allocates its resources to the various services and programs it offers in a most cost-effective way possible. The annual budget cycle begins each August and is reviewed/adopted by City Council during a special session in November.

The Budget process includes

- Coordination of citywide operating budget development activities

- Creating the Capital Improvement 5 year Program (CIP)

- Providing budgetary support and guidance to city departments

- Performing budgetary forecasting and analysis

- Engaging in long-range financial planning

Available Budgets

2026 Adopted Budget

2025 Adopted Budget

2024 Adopted Budget

2023 Adopted Budget

2022 Adopted Budget

2021 Adopted Budget

2020 Adopted Budget

2019 Adopted Budget

2018 Adopted Budget

2017 Adopted Budget

Visit the Capital Improvement Plan page for more information.

The city’s audited financial statements are prepared in accordance with generally accepted accounting principles and are independently audited by an external CPA firm. Much of the information in the audited financial statements is necessarily technical and complex. As a result, the full financial statements independently may not be particularly useful to the citizens of the city who wish to better understand city government finances.

To help bridge this gap, along with the Audited Financial Report is a Management Discussion and Analysis synopsis. This summarizes and explains the information contained in the financial statements for the last fiscal year, along with other information on the city’s finances, in easily understood terms. This summary is intended to better inform the public about their government’s financial condition, without excessive detail or the use of technical accounting terms.

This report represents the ongoing commitment of city officials to keep the citizens informed about city finances and to be accountable in all respects for the receipt and expenditure of public funds.

Available Annual Financial Reports

2025 Annual Financial Report

2024 Annual Financial Report

2023 Annual Financial Report

2022 Annual Financial Report

2021 Annual Financial Report

2020 Annual Financial Report

2019 Annual Financial Report

Visit the Event Financial Support page to learn more about the process and to apply.

Please visit the Insurance Claims page for more information and fillable forms.

Visit the People and Operational Plan page for more information

History

During the Committee of the Whole meeting on November 12, 2012, the Common Council discussed the budget impacts that included the recycling program. The Alders at that time recommended the City provide a separate container for recyclables to eliminate the recyclables being scattered in the streets. A motion was passed to add $5 per month to the Kaukauna Utilities bill for a 12-month period.

Around the same time, the City made the commitment to purchase an automated garbage truck to allow for efficiency in operations. A garbage route that had staffed two employees would now only take one staff member. The DPW area did not hire a replacement for this position in a cost saving measure through attrition.

A law change happened in 2013. This law change allowed the fee mentioned above to cover items associated with the operations such as maintenance on the truck, operating expenses, and tipping fees at the landfill to dispose of the collected garbage. With this change, the Council back in 2013 decided to make the fee permanent to help cover the cost of the service ahead of the change to the Wisconsin State Statute 66.0602(2m)(b)1.

Every house in the City has a garbage and recycling container. Regardless of the amount disposed each week, the container is emptied. Having a flat fee assessed to each home allows equality for each homeowner. Whereas, if no fee were charged and the revenue from the fee was covered through the tax rate, homes valued higher would be paying more for the same service. There is an analysis on the use of this fee below. Along with the analysis, is a frequently asked question (FAQ) that the League of Wisconsin Municipalities magazine published in the December 2020 edition.

The $5 per month shows up on each homeowners Kaukauna Utilities bill as Refuse/Recycling Fee. This fee is then passed over to the City to cover the cost mentioned above.

Garbage Collection and Recycling FAQs

Curt Witynski, JD, Deputy Executive Director, League of Wisconsin Municipalities (December 2020 Edition)

- Must municipalities provide garbage collection services? While cities and villages have traditionally and historically provided garbage collection services to their residents, Wisconsin municipalities are not required by law to do so and indeed many, mainly small, communities do not provide such a service. While large communities tend to use their own employees and equipment to collect solid waste, many medium and small communities’ contract with private haulers for such services.

- What about recycling? Must communities collect recyclables? Every city and village is required to administer their own recycling collection program or contract with another local government (also known as a responsible unit under the recycling law) to manage the recycling program within the community. Wisconsin Stat.§ 287.09.

- May a municipality provide garbage collection services for some classes of property but not others? Wis. Stat. § 66.0405 expressly provides that “cities, villages, and towns may remove…. garbage and rubbish from such classes of places in the city, village, or town as the board or council directs.” The statute further states that “Districts may be created and removal provided for certain districts only, and different regulations may be applied to each removal district or class of property. “This statute has been interpreted by the Wisconsin Court of Appeals to provide municipalities with substantial discretion in creating classifications for garbage pickup. For example, in Rubin v. City of Wauwatosa,’ the court of appeals upheld the city’s garbage program, which in 1983 involved picking up garbage from residential and commercial properties, but not industrial. Also, the city used its general fund to pay for residential garbage service and charged commercial properties a fee for the service. The city also charged residential properties special charges to pick up large items like appliances. The court upheld all aspects of the city’s program against challenges based on lack of authority and equal protection arguments. Similarly, the Court of Appeals upheld the City of Racine’s decision to not provide solid waste, pickup for buildings containing five or more dwelling units. _Carpenter v. Commissioner of Public Works of the City of Racine.’ For a more detailed discussion of these cases, see League legal opinion Ordinances & Resolutions #438.

- How can communities pay for garbage and recycling collection services? The cost of a garbage and/ or recycling collection program may be paid for out of a community’s general fund or by charging a fee against the property served. Wisconsin Stat. § 66.0627 authorizes a municipality to charge for various “current services” including “garbage and refuse disposal” and “recycling.”

- When a community shifts from paying for garbage collection services through the property tax to a fee, is there an impact on the community’s levy limit? If a municipality adopts a new fee or a fee increase for garbage collection services which were partly or wholly funded in 2013 by property taxes, the municipality must reduce its levy limit by the amount of revenue from the new fee or fee increase. See Wisconsin Stat.§ 66.0602(2m)(b). Note, that this requirement does not apply to recycling fees. The Department of Revenue (DOR), which oversees municipal compliance with the levy limit law, interprets the term “garbage collection” in Wisconsin Stat.§ 66.0602(2m) (b), to not include recycling. Therefore, if a community adopts a new recycling fee or increases an existing recycling fee, there is no requirement that it reduce its levy limit by the amount of recycling fee revenue it collects.

Monthly Garbage Collection Fee Financial Impact Example

The below analysis has been run against the 2022 budget as well as the 2025 budget. Both results were similar in the fiscal impact.

Total Annual Revenue from $5 fee: $395,500

Annual Expenses: The expenses included to maintain the Garbage collection service at the level include:

- Wages and benefit of employees collecting garbage

- Maintenance on the trucks

- Fuel

- Tipping fees to dispose at the landfill

Levy Impact: $395,500 in revenue equates to 5.62% increase in tax levy dollars. This increase in tax levy would be needed to cover the expenses mentioned above if the $5 fee was removed.

Mill Rate Impact (using the 2025 budget info): If the City only increased levy to cover the refuse/recycle fee, the levy would have increased by $395,500. This equates to a mill rate increase of 3.2% or $0.31/$1,000 over the 2025 budget. For the average house in Kaukauna valued at $225,000, this would equate to an additional tax payment of $69.75.

Expenditure Restraint Program: The 2025 Expenditure Restraint Program allowed the City to increase expenses by $928,032, and ultimately, the City increased expenses by only $926,372. By being fiscally responsible, the City benefited from this program in the form of state aid of $415,684. The increased expenses covered other needs to operate the City. If the $5 fee was removed, the expenses would need to be covered by the general fund. This would reduce the amount of funds for other services if the City desired to stay in the expenditure restraint program. The other option, if the $5 fee was removed, would be to forgo the expenditure restraint program and lose the state aid of $415,684. However, that loss must be made up through the levy or some other revenue stream.

Levy Limit Impact: The City of Kaukauna is limited by what levy increase can happen without a referendum. The 2022 budget had an allowable levy limit increase of $616,472.